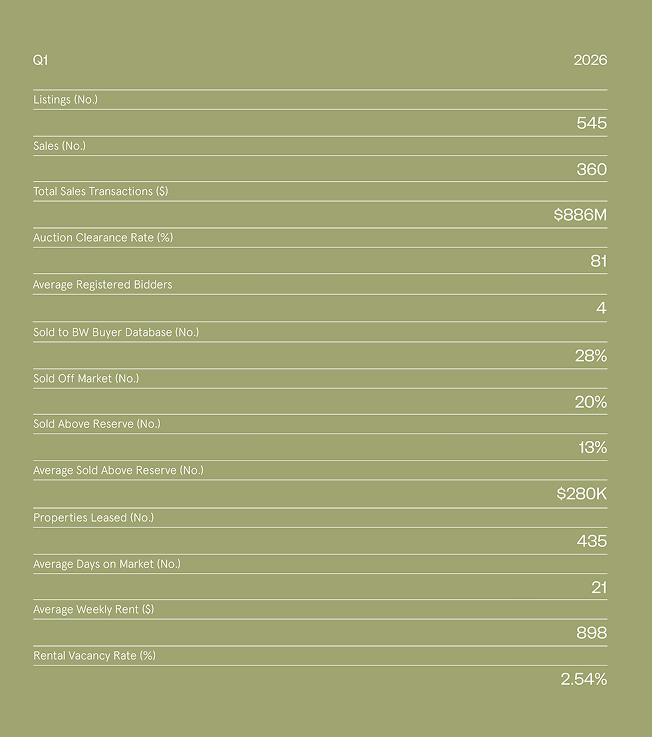

Q1 2026

Author

BW Creative

Photography

Ryan Unwin

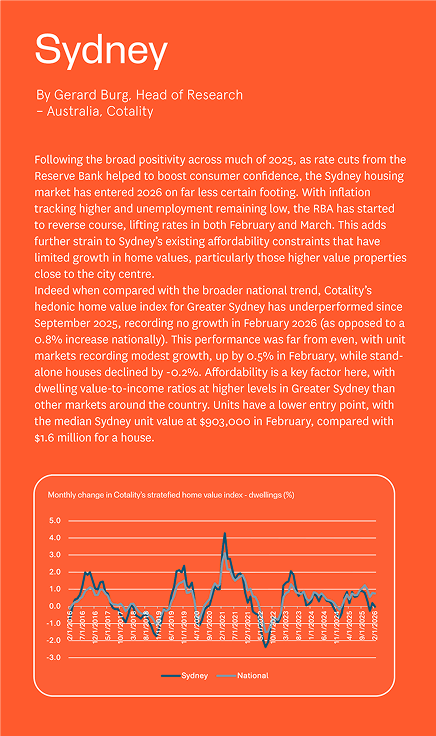

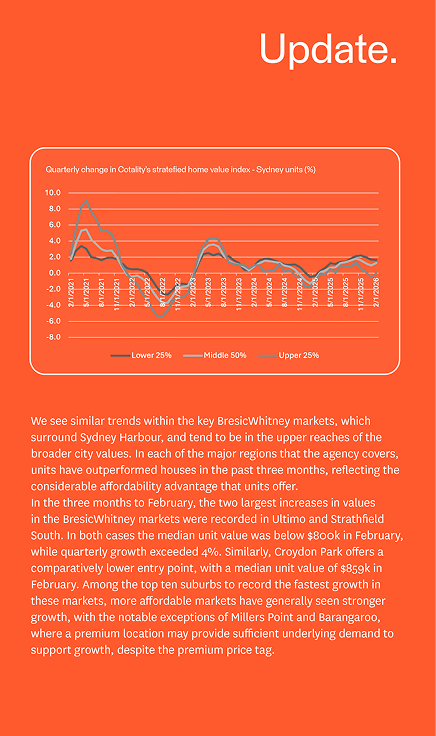

Sydney property in Q1 2026 has been a patchwork - activity shifting frequently, conditions varying across price points, and the forces shaping decisions anything but straightforward. Complexity remains, but it doesn't diminish the fundamental demand for property in this city. The path looks different this quarter. The considerations do too.

Economic headwinds, speculation around capital gains tax changes adding to seller uncertainty, a rising rate environment, and an increasingly complex global backdrop have all played a role. Buyers and sellers are responding in ways the data is beginning to capture - auction clearance rates sitting at approximately 55% across wider Sydney by late March, down from 65% year-on-year, [Placeholder: % of homes sold prior to auction - Finance to provide], [Placeholder: volume sold and/or listed YOY - Finance to provide], a growing proportion of sales transacting off-market, and a departure from the seasonal peaks that have traditionally defined this market. Supply is also rising in Sydney, with more stock on market contributing to the clearance rate story - this is a buyer behaviour story as much as a supply one. In the rental market, supply constraints show no sign of easing, and government efforts to boost stock and ease planning pathways have yet to produce meaningful uplift.

Affordability is becoming a more structural issue - not just rate driven. With approximately 62% of income now required to service an entry-level Sydney home, and the cost of other goods and services continuing to rise, the pressure on buyers extends well beyond the cash rate. [Placeholder: if data supports it, add specific reference to days with highest sales volume showing unusual seasonal activity - Finance to provide]

Resilience remains - but the complexities faced by buyers and sellers, tenants and owners, will be the defining conversation for much of the 2026 calendar year. Keep reading for an update on where opportunities lie, where constraints remain, and where the market is heading - alongside a comprehensive update from exclusive data partner, Cotality.

"Sydney property in 2026 is asking more of everyone in it. More patience, more preparation, more clarity on what's actually driving conditions. The Quarterly exists to give you that." - Will Gosse, BresicWhitney CEO

CGT uncertainty is influencing seller decision-making – owners sitting on significant gains are pausing, weighing up the cost of selling now versus holding. Yet the data tells a more nuanced story. [Placeholder: Cotality/Domain Q1 stock data] shows that the amount of stock launched onto the market over Q1 has remained substantial – sellers who moved early were motivated by the momentum of last year and a desire to optimise sale prices while rates were held. Supply is rising in Sydney, and more stock on market is part of the clearance rate story – but this isn't primarily a supply problem. It is a buyer behaviour story.

What has occurred concurrently is that more complexity has entered the market. Geopolitical pressures – including a conflict reshaping global energy markets – and two consecutive rate rises have compounded an imbalance between buyer hesitation and an elevated number of properties available. Active buyers now have greater choice and less urgency to stretch on price, and that is showing up in auction clearance rates and overall sales volumes. By the end of Q1, negotiations were requiring more careful handling to bring buyer and seller together in a reasonable timeframe – agent execution and seller willingness to meet the market have become increasingly important.

This isn't one market right now. Below $1.5m there is genuine competition - buyers who are motivated, financing in place, ready to move. Above $2m, sellers are working harder and waiting longer to bring buyers to the table. Knowing which market you're in changes the strategy entirely.

And yet the underlying demand is there. [Placeholder: BW average buyers met per week over Q1 - Finance to provide] – a figure that speaks to the level of active interest in the market even as transactions take longer to come together. Foot traffic has remained healthy. The buyers are present. [Placeholder: if data supports it, add nuance around a specific price point or property type that is still transacting quickly – OK to omit if data doesn't clearly support this.]

Everything in this market is connected – and that is perhaps the most important thing to understand about Sydney property right now. CGT doesn't sit in isolation. Interest rates, cost of living pressures, geopolitical context, and broader economic sentiment are all part of the same picture, and housing is as exposed to that picture as any asset class. The RBA has now raised the cash rate twice in 2026, taking it to 4.1% - and with inflation not expected to return to the middle of the target band until 2028, conditions are likely to remain as they are for the coming months. Clearance rates across wider Sydney fell to approximately 55% by late March, down from 65% year-on-year – a tangible measure of how that pressure is being felt. This isn't a market waiting for a single catalyst to shift. It is a market learning to move within a new set of parameters.

Affordability is increasingly structural - not just rate driven. Approximately 62% of income is now required to service an entry-level Sydney home, and as the cost of other goods and services rises alongside borrowing costs, the affordability challenge extends well beyond the cash rate alone.

The opportunity window

For some owners, the current environment is accelerating decisions rather than stalling them. We have seen this in previous cycles - when complexity increases, the buyers and sellers who stay closest to the market tend to be the ones who move most effectively. Greater education, greater proximity to what is actually happening, creates the confidence to act when others are hesitating. With further rate hikes anticipated in May, some buyers are motivated to move now and secure financing before conditions tighten further. Buyers who have been sitting on the sidelines may find this creates selective opportunity - met, increasingly, with a willing seller who is ready to meet the market. Easter through late autumn remains a critical window. How activity comes to life across the broken calendar of April will help set the tone for the second half of the year.

“The market hasn't stalled. The buyers are there. What's changed is the weight of the decision – and that weight is real. Two rate rises in two months, a conflict reshaping global energy markets, tax settings still unresolved. People are thinking harder before they move. That's rational. But thinking harder and waiting indefinitely aren't the same thing – and for buyers watching their borrowing capacity, the cost of waiting is already showing up in the numbers.” – Will Gosse, BresicWhitney CEO

The efficacy of off-market sales is nothing new - but what is new is how well understood and accepted off-market, or off-portal, sales have become. Historically used to surface buyer interest before an on-market campaign, they are now accepted as an end-to-end solution by many buyers and sellers, offering diversity, discretion, and first access to new properties. Part of BW's DNA since inception, it is a shift expected to become increasingly offered across the industry - given the continued need for choice and options in the current economic landscape, where the rising cost of listing a property is a real consideration for many vendors.

A Cotality report confirms that data ownership ranks as a key priority across the industry, with 77% of respondents rating greater control of customer data as highly important - yet this intent is not always reflected in execution. Only 28% of agencies reported listing properties on their own website before publishing on portals, while a larger share continue to prioritise portal-first distribution. [Hyperlink [BD1] to Cotality report to be added] Most importantly, it is about agencies meeting their customers on the platforms they are using. Survey responses indicate a growing awareness of changes in how customers discover property, engage with agencies, and move through digital channels - suggesting a continued focus on digital capability and customer communication in 2026, with real estate agencies at different stages of aligning intent with operational practice.

BW has prioritised its own website and database first since the beginning - connecting buyers directly before going to market broadly. This approach reflects a belief that the best outcomes come from relationships, not just reach. It also extends to how BW approaches price guide transparency and the long-term servicing of both buyers and sellers - advertising price guides that reflect genuine market positioning, rather than optimising for portal traffic at the expense of trust on either side of the transaction. Approximately 20% of BW sales transact off-market. In February, 18% of transactions occurred exclusively through bw.com.au, up from 13% in January - March figures to follow. [Placeholder: 2-year, 5-year and 10-year comparison of % of BW sales completed off-market - Finance to provide. This anchors the trend with historical context.]

The message is not that off-market is always the right answer - it is that choice, diversification and discretion matter. At a time when complexity and nuance in the market are high, having access to every avenue is what sets the right outcome apart from a good one.

“Off-market isn't a workaround. It's what happens when relationships are built before the campaign starts. The outcome is different - cleaner, faster, less exposed. In a market where execution matters more than it did a year ago, that difference is only becoming more relevant.” - Will Gosse, BresicWhitney

Does off-market deliver? [Listicle - formatting TBC with Creative team]

Off-market isn't one thing. It's a first look before a campaign launches. It's a buyer already in the database when the right property comes up. It's a transaction that completes before a sign goes up. The common thread is relationships built before the moment of sale – and outcomes that reflect it.

[Placeholder: anchor with 2, 5 and 10-year comparison of % of BW sales completed off-market – Finance to provide. Frame as: "Over the past X years, approximately X% of BW sales have transacted off-market. In February 2026 alone, 18% of transactions occurred exclusively through bw.com.au, up from 13% in January."]

What this looks like in practice

· The campaign that kept going A strata warehouse conversion in the Inner West – five dwellings, one site. The first sold at auction. The remaining four transacted off-market off the back of that campaign, with buyer demand drawn from surrounding suburbs broadened by new local infrastructure. Total sales return: $13.9m from a $3.55m purchase in 2023.

· The buyer who was already there A property in the Inner West. A buyer encountered it at the photoshoot and exchanged that afternoon. No open homes. No extended campaign. The right buyer was already in the network – and ready to move.

· Depth of demand at every price point A sub-$800k apartment in the Inner City drew 30 inspections over 10 days – all from the BW database, before the property was broadly advertised.

· Speed when it matters An Eastern Suburbs property – buyer identified online on day one, viewed privately before the first open home, sold in 8 days.

· Clean and unconditional A Lower North Shore apartment – sold off-market, unconditional. No extended negotiation, no conditions, no uncertainty.

· A conversation, not a campaign A Hunters Hill property managed and leased through BW was introduced to buyers off-market while it remained tenanted. A buyer's agent made enquiries, the agent called the owner, and a $1,000,000 sale came together. The buyer was country-based and never needed to attend in person.

[BD1]https://www.cotality.com/au/insights/articles/housing-confidence-remains-high-despite-rising-economic-risks

Time in the market consistently outperforms attempts to time the market - and in 2026, that case has rarely been easier to make. Sydney property has delivered sustained value over the long term not because people bought and sold at precisely the right moment, but because they participated. [Placeholder: Cotality 5-year median house price data to anchor this point - data due 1 April. This is load-bearing for the section's argument and should lead once available.]

What does that mean in practical terms for buyers and sellers navigating 2026? For buyers, each month of hesitation in a rising rate environment carries a real cost - not just in sentiment, but in borrowing capacity. For sellers, the traditional logic of holding for spring is being tested by a market that no longer waits for the calendar. The best time to act is when the property is well-presented, the strategy is right, and the right people are around you - not when the season says so.

“The data will tell you when the best days to transact were – and they're rarely the days anyone predicted. What we're seeing is buyers and sellers acting on their own terms, their own timing, their own readiness. The seasonal premium is less reliable than it's ever been. A well-prepared property with the right people behind it can transact in any month. That's not a prediction. That's what the last twelve months have shown us.” - Will Gosse, BresicWhitney

What the data is telling us [Note: if this is the meatiest part of the section - lead with it if the data is strong enough once received from Finance. If data is thin, keep it brief and let the BW perspective carry the section.]

[Placeholder: 5 highest days of property sales in the last 12 months - Finance to provide. This is central to the section's argument.] [Placeholder: YOY comparison - are peak transaction days shifting away from traditional seasonal windows? The answer will sharpen or soften the angle.] [Placeholder: Do public holidays and school holidays show a measurable dip in activity - or not? If the data shows they don't, that's a strong editorial proof point.]

BW is observing a sustained shift in buyer behaviour – transactions are happening year-round, driven by personal readiness and the right property coming to market rather than a date in the diary. Life events don't follow a seasonal schedule. Neither does financial urgency. With two rate rises already in 2026 and further increases possible, some buyers are acting on financial timing as much as personal timing – wanting to move before conditions tighten further. Local buyer movement is increasingly driven by opportunity, not season.

What to expect for the rest of 2026

“Complexity creates opportunity for the people who stay closest to the market. That's been true in every cycle we've navigated. The buyers and sellers moving well right now aren't waiting for certainty. They understand the conditions. They're ready when the right moment presents.” – Will Gosse, BresicWhitney CEO

Easter through late autumn is a critical window – if transaction momentum doesn't build across this period, it may set a more conservative tone heading into winter. Notably, the rental market is telling a similar story: the seasonal softening that typically offers tenants some winter reprieve may not materialise this year, suggesting that Sydney's property market – sales and rental alike – is increasingly moving to its own rhythm rather than the calendar's.

For buyers, the recommendation is clear – stay close to the market, understand your position, and be ready to move when the right property presents. Waiting for a clearer signal in a rising rate environment is itself a decision with consequences – for buyers watching their borrowing capacity, the cost of waiting is already showing up in the numbers. For sellers, the spring premium may be less reliable than it once was. A well-presented property with the right strategy behind it can transact in any month.

The big picture

The rental market has tightened again. Vacancy is back to 1.2%, a figure that reflects the persistent supply-demand imbalance that continues to define Sydney's rental landscape. Housing supply remains a critical and unresolved issue – structural, not cyclical – and there is no quick fix in sight. Government efforts to boost supply and ease planning pathways over the last six to twelve months have yet to produce any immediate uplift.

[Placeholder: Cotality vacancy rate and supply data for Q1 to complement the 1.2% figure. Domain rental report and REINSW rental insights to be incorporated - Amy to send through.]

New rental stock is not entering the market at a rate that meets demand. Rising interest rates – with the cash rate now at 4.1% following two hikes in 2026 – have shifted the calculus for investors considering new acquisitions, further constraining the pipeline of available rental properties. Affordability pressures extend beyond borrowing costs – as the cost of living rises more broadly, more people are remaining in the rental market for longer, sustaining and deepening demand at exactly the moment supply is most constrained.

On the ground

Discerning tenants continue to prioritise location, connectivity, walkability and lifestyle amenity – and the continued evolution and investment in Sydney's lifestyle markets means this demand is unlikely to ease over the medium term. When the right property presents, tenants move decisively.

Typically, winter brings some seasonal softening – a period of reprieve for tenants. This year, that relief may not come. Sydney's rental market, much like its sales market, is increasingly moving to its own rhythm rather than the calendar's.

For landlords and investors with well-located assets, sustained demand continues to underpin confidence and performance, even as holding costs increase.

“A well-presented home in a lifestyle suburb close to the city doesn't sit for long right now. We're seeing multiple applicants moving quickly and decisively – tenants know what they want, and when the right property comes up, they don't hesitate. Our team is feeling that demand every day. Vacancy is back to 1.2% and the signs that would typically point to a winter reprieve aren't there this year. Supply remains the critical issue, and until that shifts in a meaningful way, I don't expect conditions to ease.” – Chantelle Collin, BresicWhitney, Head of Property Management

testtetete